There is a massive, glaring problem at the heart of mainstream FIRE (Financial Independence Retire Early) content: Much of mainstream FIRE content presents achieving FIRE as a result of extreme savings rates that are utterly divorced from realistic incomes and real-world expenses.

This type of content typically is peddled by out-of-touch men who make bloated salaries and speak as if their massive savings rate is merely a function of their iron discipline and austere frugality — not their income. Thus, they speak as if their advice applies to all income brackets — as if you too can save 85% of your income if you simply try hard enough.

Emphasizing savings rate over income

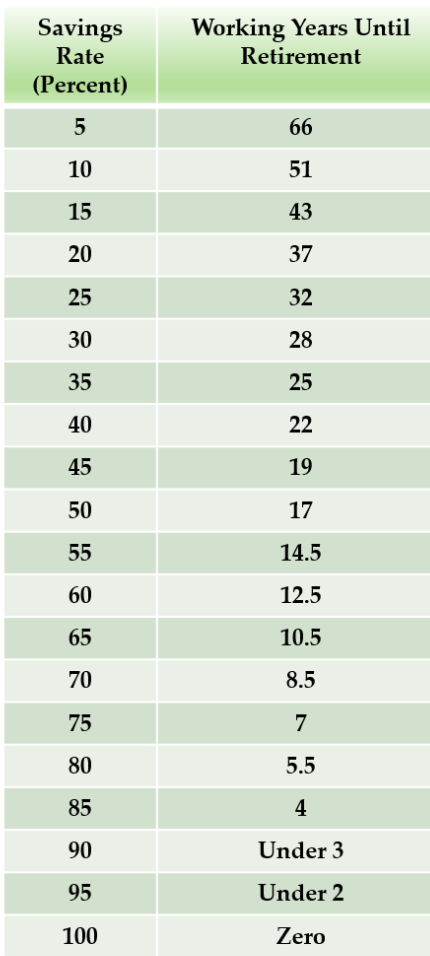

For Mr. Money Mustache, a popular personal finance blog with a focus on the FIRE movement, achieving FIRE is just a matter of “simple math” — even if that math doesn’t add up in the real world of the low wage crisis. In “The Shockingly Simple Math Behind Early Retirement,” he presents the following chart, saying, “Here’s how many years you will have to work for a range of possible savings rates, starting from a net worth of zero:”

The problem with this chart is that it’s not grounded in an understanding of what income real people — especially women — actually make.

According to a 2024 study by Oxfam, 23% of U.S. adults earn less than $17 an hour as of 2024. This percentage climbs even higher if you take into consideration factors like gender and race: “When looking at gender alone, 27.6 percent of working women earn low wages compared to 19 percent of working men.”

Here is a breakdown of more statistics about the crisis of low wages from Oxfam’s study:

- In 21 states, 30–40% of all women earn below $17 an hour in 2024.

- Only 17% of white men earn below $17 an hour, whereas 25% of white women earn below $17 an hour. In 12 states, 30–40% of white women earn below $17 an hour. There are zero states where 30%+ of white men earn less than $17 an hour.

- Nationwide, 35% of Black women earn below $17 an hour. In 13 states, 40–50% of Black women earn below $17 an hour. In three states, 50–60% of all Black women earn below $17 an hour.

- Nationwide, 39.9% of all Latina or Hispanic women earn below $17 an hour. In 31 states, 30–40% of working Latina or Hispanic women earn below $17 an hour. In seven states, 40–50% of Latina or Hispanic women earn below $17 an hour. In four states, over 50% of all Latina or Hispanic women earn below $17 an hour.

$17 an hour is about $35,360 gross per year — assuming 2 weeks of unpaid vacation per year and a 40-hour work week. But Mr. Money Mustache’s “The Shockingly Simple Math Behind Early Retirement” chart refers to take-home pay, which would be roughly $27,000 a year after taxes — depending on what state you live in. And we haven’t even factored deductions for health, vision, and dental insurance into this analysis.

According to Mr. Money Mustache’s chart, if someone saves 95% of their income for less than 2 years, then they will be able to retire early. To be generous, let’s round it up to a solid 2 years. If you’re one of the many women who makes about $27,000 a year after taxes and is somehow able to save 95% of her income for a solid 2 years, she will have $51,300 saved after those 2 years, not including compound interest or inflation.

Assuming that somehow you invest 95% of your net income (which turns out to be $25,650 annually) for 2 years with a 5% compound interest rate — which is the assumption that Mr. Money Mustache’s chart makes — the account value would be about $52,582.50 after 2 years.

That’s it! According to Mr. Money Mustache, you’re ready to retire! You just have to limit your withdrawals to 4% of your portfolio balance. Wait, what’s that, you say? What do you mean, you can’t live off of some odd $2,103 a year for decades?

You see, Mr. Money Mustache’s chart rests upon the assumption that you can live off of 4% of your retirement account balance per year. That’s a massive problem — just because the math might work in theory doesn’t mean that this is good advice that will actually work in the real world. In order for the 4% rule to work, it has to track with realistic incomes and realistic living expenses.

The reality in this scenario is that you would completely run out of money before 2 years, assuming you have a relatively low cost of living of about $2,000 per month.

Let’s try again with a different savings rate.

Let’s assume you are part of that group of 30–40% of women across 21 states who earn less than $17 per hour — but let’s round it up to $17. Let’s assume that somehow you’re magically able to save 80% of your after tax income over the course of 5.5 years: That’s about $122,301.08 considering Mr. Money Mustache’s assumption of a 5% rate of return.

Or maybe you’re able to save 65% of your income for 10.5 years. That same income and rate of return yields $226,193.25. Better, but still not nearly enough to retire on — let alone retire significantly early.

This analysis shows that, when it comes to FIRE, your income is just as important — if not more so — than your savings rate.

Not accounting for the cost of living.

The third problem with “The Shockingly Simple Math Behind Early Retirement” is its utter disregard for realistic costs of living.

Mr. Money Mustache makes the assumption that you can just retire right now if you have zero living expenses. He says, “If you are spending 0% of your income (you live for free somehow), and can maintain this after retirement, you can retire right now. So your working career can be Zero.” If you’re homeless and you steal food and clothes from dumpsters, that doesn’t mean you’ve retired.

Other statements he makes completely disregard the cost of living. Mr. Money Mustache says, “If want to retire within 10 years, the formula is right there in front of you — simply live on 35% of your take-home pay,” as if this is something that just anyone can do.

When over one fourth of all working women earn less than $17 an hour, which is roughly 27–29k after taxes — not including deductions for health, dental, or vision insurance — this advice is not actionable or realistic: 35% of 27k is $9,450.

Housing

The median rent for a studio apartment in 2025 in the United States is $881 per month (or $10,572 per year), and the median rent for a one-bedroom apartment in 2025 in the United States is $950 per month (or $11,400 per year), according to the a comprehensive dataset of median rent prices in thousands of counties across the U.S., published by the U.S. Office of Policy Development and Research.

Considering the cost of living, if you’re like one of the many low-income women in the United States, you can’t afford to restrict your spending to 35% of your income.

Even if you got a roommate and paid half ($582.50/month or $6,990/year) of the median rent cost for a two-bedroom apartment ($1,165/month or $13,980/year), you’d still be left with $2,460 out of the original $9,450— and we haven’t even factored in the cost of food yet.

Food

The U.S. government reports that a thrifty grocery budget for women aged 20–50 is $247/month, or $2,964/year, as of January 2025. It’s too bad you only have $2,742 after housing. And you still haven’t factored in costs for health insurance, utilities, transportation, copays, cell phone service, and other basic necessities.

For the women who earn less than $17/hour, living on 35% of their income simply isn’t possible.

Content by the wealthy, for the wealthy

In case you thought that the example of the the homeless man who saves 100% of his income or the woman who saves 95% of her income for 2 years were uncharitable and unfair interpretations of Mr. Money Mustache’s ethos, know that he explicitly states that “The most important thing to note is that cutting your spending rate is much more powerful than increasing your income.”

And although Mr. Money Mustache says that “Your savings rate is determined entirely by these two things: How much you take home each year” and “how much you can live on,” this is the start and end of his conversation around a realistic relationship between income and cost of living.

For Mr. Money Mustache, this is merely a throwaway comment — when you look at the content of “The Shockingly Simple Math Behind Early Retirement” as a whole, it’s more than clear that a realistic analysis of income and costs of living have zero place in his content.

For Mr. Money Mustache, achieving FIRE is just as simple as following a formula that exists in a vacuum. For him and countless other FIRE devotees, the savings rate formula — not realistic incomes, realistic costs of living, realistic withdrawal amounts, or total retirement account balance — is the most important component of your FIRE journey; the tacit assumption behind this content seems to be that you too are an upper-middle class person, and probably a man, given that 75% of high-income earners are men.

Only someone who makes well above the median income — and assumes their audience can do the same — would make a chart showing that you too can retire early if you just save 85% of your income for 4 years.

Statements like “The most important thing to note is that cutting your spending rate is much more powerful than increasing your income,” and “If want to retire within 10 years, the formula is right there in front of you — simply live on 35% of your take-home pay” are the kind of delusions that could only be propagated by someone who is utterly out of touch with realistic incomes and realisitic living expenses.

And Mr. Money Mustache is far from being the only out-of-touch personal finance guru: The internet is rife with content in which upper middle class and wealthy men present their savings rate as the result of their iron will and austere frugality rather than a result of their almost six- or seven-figure salaries — from the man who saved 82% of his income to the man who saved 99% of his income to the man who saved 70% of his income.

Other FIRE bloggers are just as out of touch: Financial Samurai, one of the largest independently-owned personal finance blogs, regularly says outlandish things like “10 million or more” is the ideal net worth to retire on and “A $20 million net worth is achievable with enough time and discipline.“

This kind of content that pretends that high incomes are the norm, completely disregards the crisis of low wages in America, and presents extreme savings rates as a product of your own will rather than the result of a bloated salary is not just exclusionary to low-income and median-income earners — it completely erases them.

When FIRE bloggers write content that’s utterly divorced from reality, this just turns regular people off to the idea of actively striving for financial independence, and that’s a huge problem considering the median retiree has just $142,500 saved, and the median retired woman has just $100,000—well below what’s needed to ensure a comfortable retirement.

That’s why FIRE bloggers should stop fetishizing extreme savings rates that are divorced from reality and start making content that makes striving for FIRE more accessible and welcoming to normal people in low and median income brackets — not just high-income ones.

Low-income and median-income people need resources that make the conversation around financial independence inclusive and accessible to their income level because financial independence is something that everyone needs. This blog, FIRE for Normal People, strives to be that resource.