If you don’t earn a high income, you might believe you have too little money to make investing matter. However, this belief is not only false—it actively hurts your finances and can cause you to miss out on tens or even hundreds of thousands of dollars or more in future investment income. Investing on a low income is actually possible and you can build wealth on a low income, especially if you harness your most valuable wealth-building tool: time.

Don’t let an all-or-nothing mindset stop you from making progress toward your financial goals. Some personal finance experts advise investing about 20–25% of your income if you want to achieve financial abundance. While that’s often not achievable for low-income earners and even some median-income earners, you can still make a powerful contribution to your retirement account if you increase your investment contributions by just 1% of your income—no matter your current income level.

What does investing 1% more do for your financial future?

The Money Guy’s free resource What 1% More Can Do for You details just how powerful investing 1% more of your income can be. This chart shows how much that 1% of your income could grow by the time your reach age 65:

Let’s break down what this chart could mean for you:

- If you invest 1% more of your income starting at age 22, that money could grow to over 8x your initial contribution if you retire at 65.

- If you invest 1% more of your income starting at at age 28, the amount you invested could grow to over 5x your initial contribution if you retire at 65.

- If you invest 1% more of your income starting at age 30, that 1% could grow to 4.7% by the time you retire. That 1% has the potential to grow to almost 5x more than what you originally invested.

- If you invest 1% more of your income starting at age 35, that 1% could grow to 3.3% by the time you turn 65. In other words, your investment contribution has the potential to triple.

- If you invest 1% more of your income starting at age 42, that amount could double by the time you reach 65.

The benefit of investing 1% more is clear: Depending on the age you start investing, by the time you retire, you could have almost two to nine times more money than that initial 1% investment.

Adopt the mindset that every dollar counts.

Investing 1% more might not immediately make or break your financial situation, but it can be a huge catalyst for positive change over the long term, especially if you struggle to see investing as something that’s accessible for you.

If you’re struggling to reach a 20–25% investment rate to achieve financial abundance, gradually increasing your investment contributions by 1% more can help nudge your way to this goal. Investing 20–25% may not be possible for you right now, but smaller goals can help you inch your way to that 20–25% investment rate:

- If you’re starting from zero and your budget is tight, try just starting with 1% and then increasing your contributions as you’re able. Note: I recommend setting a calendar reminder to periodically check in on your finances to see if you can increase your investment contributions because you don’t want to stop at just 1%. Again, the general principle is that you want to be investing at least 15% if not 20–25% for retirement.

- If you’re already investing 5%, try increasing your contributions to 6%.

- If you’re already investing 15% (a GREAT starting place), try increasing your contributions to 16%.

No one can retire only by investing only 1% of their income, but increasing your investment contributions by 1% could still make a substantial difference to your future finances. Not investing 1% more of your income means you might miss out on tens of thousands of dollars in future investment income—even if you’re a low-income earner.

The truth is that you don’t need to have hundreds of dollars in extra income in order for investing to matter. The key ingrediant for building wealth is the amount of time that your money is invested.

That’s why investing 1% more of your income can have such a powerful impact in your finances. That’s also why it’s such a huge mistake to put off investing because you don’t think you have enough money for investing to matter.

Saving 1% more can make a dent in your investment goals, even if you are a low-income or median-income earner.

Let’s see what that 1% increase looks like using hard numbers.

Although it’s likely that you will get a significant pay increase over the long-term, the following examples don’t assume that you’re going to get a salary increase because the reality for most low-wage and median-wage workers is that they don’t get predictable pay raises if they stay at their current job, and when they do, the pay raises often don’t keep up with inflation.

Switching jobs is by far the most reliable way to get a pay increase, and because each person’s financial journey is unique to them, it’s impossible to make examples that will predict your income trajectory, so we’ll assume that your income remains stagnant in these examples.

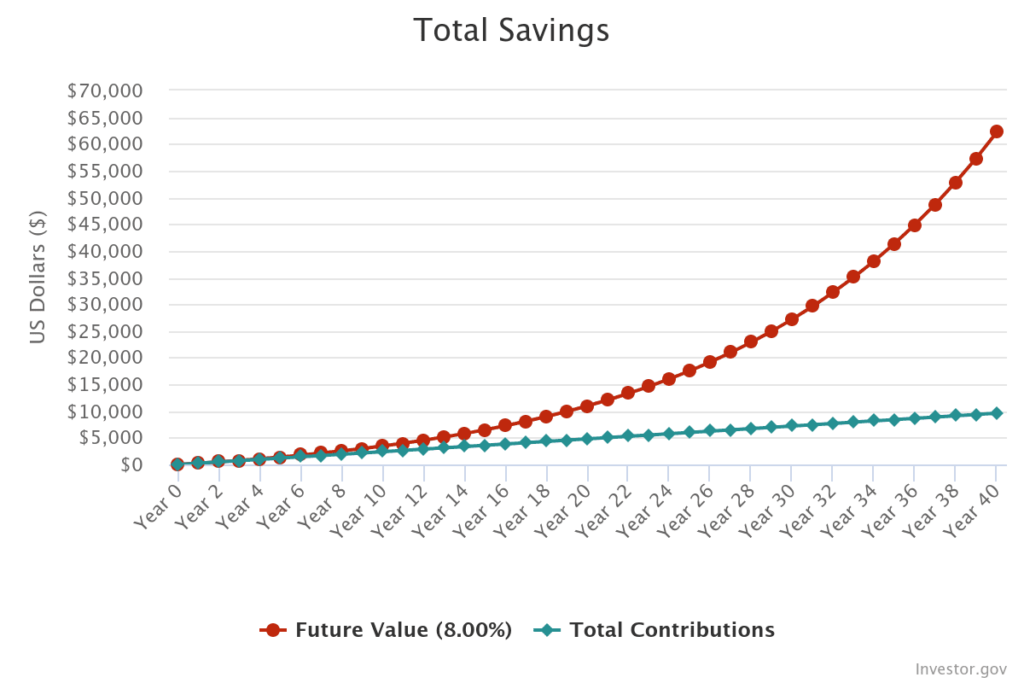

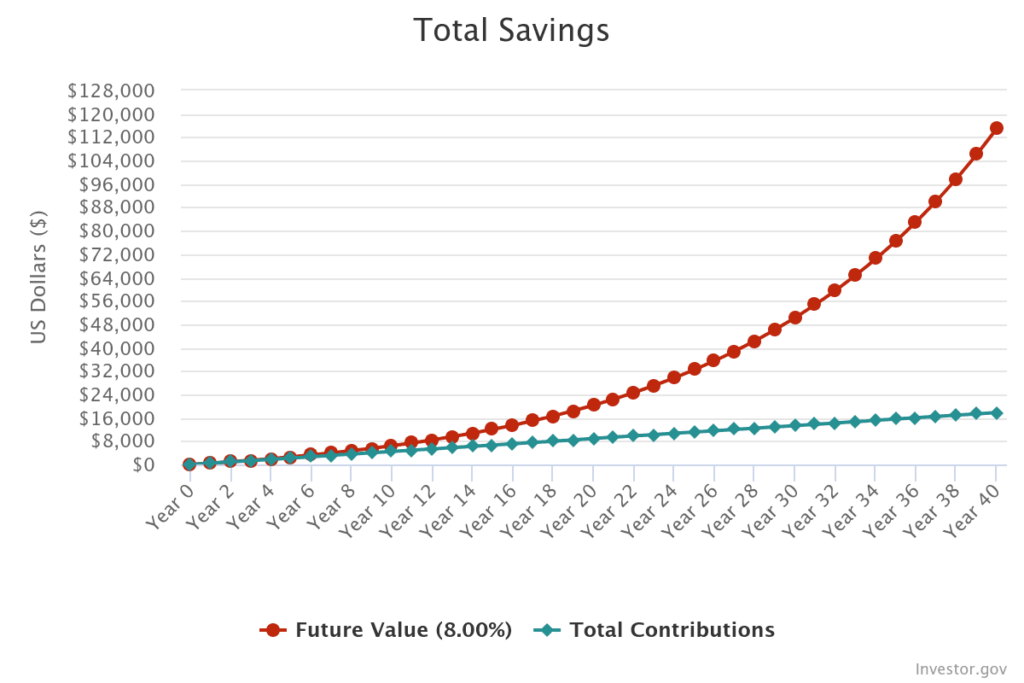

Investing 1% more on a $25,000 income

If you earn $25,000, you are probably more focused on just getting by and trying to save for emergencies than investing.

But on the off chance that you live in an area with a super low cost of living and actually do have some extra money left over each month, you might start with investing 1% of your annual income if that’s all that you can afford to invest. That’s just $250 per year or about $20.84 per month.

Here’s how much you could potentially have if you invest 1% more, which is just $20.84 per month:

- After 25 years, you will have contributed $6,000, and your money could grow to $17,545, potentially earning you $11,545 in compound interest.

- After 30 years, you will have contributed $7,200, and your money could grow to $27,187, potentially earning you $19,987 in compound interest.

- After 35 years, you will have contributed $8,400, and your money could grow to $41,356, potentially earning you $32,956 in compound interest.

- After 40 years, you will have contributed $9,360, and your money could grow to $62,173, potentially earning you $52,813 in compound interest.

Notice that there’s very little difference between the amount that you contributed over 25 years ($6,000) and the amount that you contributed over 40 years ($9,360), but the amount of compound interest you earn skyrockets the longer that that that money is invested.

The reason for this growth is that time is more important that money when it comes to building wealth—that’s why you can still build wealth even if you earn a low income. Even if you’re not able to invest yet, know that any investing that you’re able to do regardless of your level of income could make a noticeable difference to your financial future.

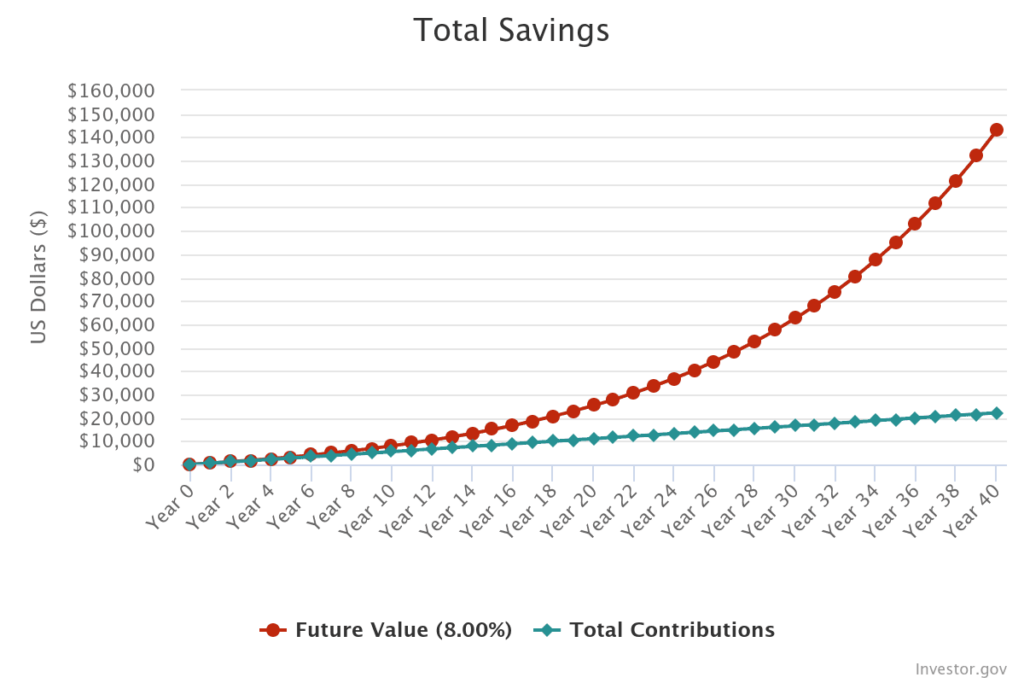

Investing 1% more on a $30,000 income

If you earn $30,000 a year, you’re probably still in survival mode and are struggling to save for emergencies, let alone invest. However, if you’re one of the few individuals that does have some money left over after after your necessary expenses, any investments you make at this income level could still be worthwhile.

Here’s how much you could have if you invest 1% more of your income, which is $300 a year or $25 a month, with an 8% rate of return:

- After 25 years, you will have contributed $7,500, and your money could grow to $21,931, potentially earning you $14,431 in compound interest.

- After 30 years, you will have contributed $9,000, and your money could grow to $33,984, potentially earning you $24,984 in compound interest.

- After 35 years, you will have contributed will have contributed $10,500, and your money could grow to $51,695, potentially earning you $41,195 in compound interest.

- After 40 years, you will have contributed $12,000, and your money could grow to $77,716, potentially earning you $65,716 in compound interest.

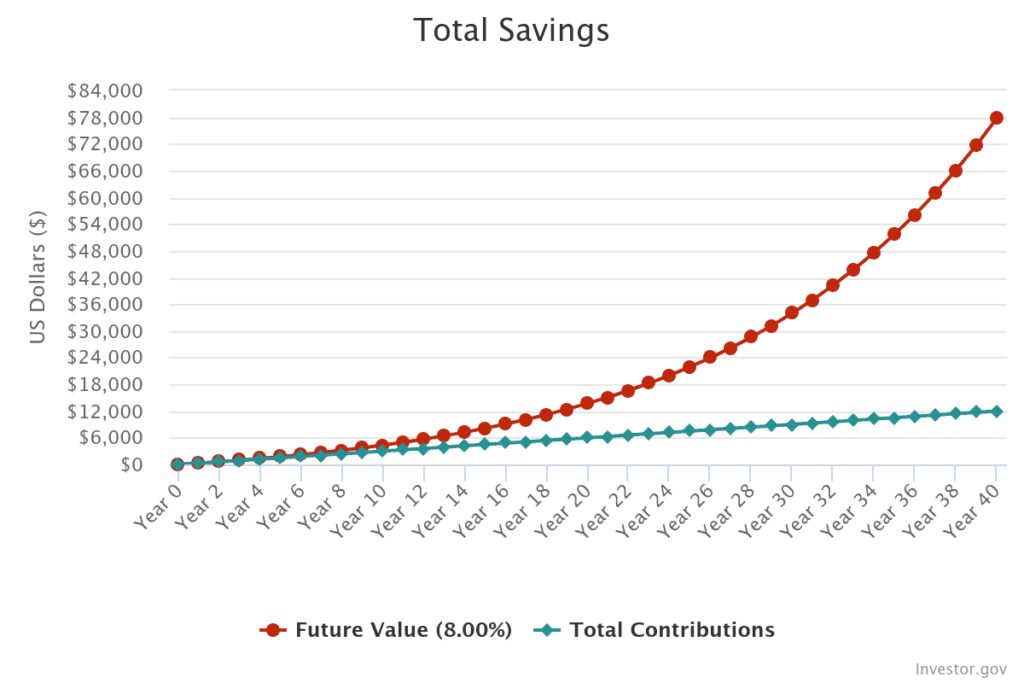

Investing 1% more on a $35,000 income

If you earn $35,000 a year, investing 1% more of your income could still make a difference to your financial future.

Here is how much your money could potentially grow if you invest 1% more of your income, which is $350 per year or about $30 per month, with an 8% rate of return:

- After 25 years, you will have contributed $9,000, and your money could grow to $26,318, potentially earning you $17,318 in compound interest.

- After 30 years, you will have contributed $10,800, and your money could grow to $40,781, potentially earning you $29,981 in compound interest.

- After 35 years, you will have contributed $12,600, and your money could grow to $62,034, potentially earning you $49,434 in compound interest.

- After 40 years, you will have contributed $14,400, and your money could grow to $93,260, potentially earning you $78,860 in compound interest.

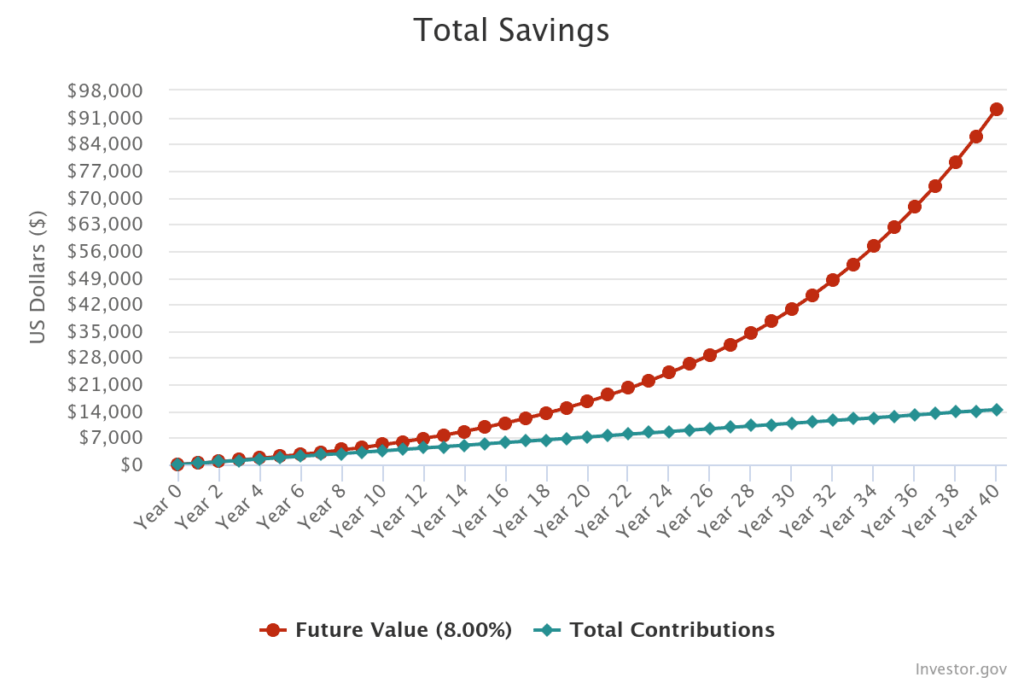

Investing 1% more on a $40,000 income

If you earn $40,000 a year, hopefully you can manage to invest some of your income. At this income level, increasing your investment contributions by 1% could make a massive difference to your financial future, especially if you start investing early.

Here’s how much your money could potentially grow if you invest 1% more of your income, which is $400 per year or about $34 per month, and get an 8% rate of return:

- After 25 years, you will have contributed $10,200, and your money could grow to $29,827, potentially earning you $19,627 in compound interest.

- After 30 years, you will have contributed $12,230, and your money could grow to $46,219, potentially earning you $33,989 in compound interest.

- After 35 years, you will have contributed $14,280, and your money could grow to $70,305, potentially earning you $56,025 in compound interest.

- After 40 years, you will have contributed $16,320, and your money could grow to $105,695, potentially earning you $89,375 in compound interest.

Investing 1% more on a $45,000 income

If you earn $45,000 a year, you should be excited about what investing 1% more of your income could do for your financial future. Here’s how your money could possibly grow if you invest 1% more of your income, which is $450 per year or $37.50 per month, and get an 8% rate of return:

- After 25 years, you will have contributed $11,100, and your money could grow to $32,459, potentially earning you $21,359 in compound interest.

- After 30 years, you will have contributed $13,320, and your money could grow to $50,297, potentially earning you $36,977 in compound interest.

- After 35 years, you will have contributed $15,540, and your money could grow to $76,508, potentially earning you $60,968 in compound interest.

- After 40 years, you will have contributed $17,760, and your money could grow to $115,021, potentially earning you $97,261 in compound interest.

Investing 1% more on a $50,000 income

If you make $50,000 a year, you should be excited about how your money could grow if you just invest 1% more of your income. If you invest $500 per year or about $42 per month, and you get an 8% rate of return, here’s how your money might grow:

- After 25 years, you will have contributed $12,600, and your money could grow to $36,845, potentially earning you $24,245 in compound interest.

- After 30 years, you will have contributed $15,120, and your money could grow to $57,094, potentially earning you $41,974 in compound interest.

- After 35 years, you will have contributed $17,640, and your money could grow to $86,847, potentially earning you $69,207 in compound interest.

- After 40 years, you will have contributed $20,160, and your money could grow to $130,564, potentially earning you $110,404 in compound interest.

Investing 1% more on a $55,000 income

If you make $55,000 a year, just a 1% increase in your investment contributions could possibly mean a huge boost in future investment income. Here’s how much your money might grow if you invest 1% more of your income, which is $550 per year or about $46 per month, and you get an 8% rate of return:

- After 25 years, you will have contributed $13,800, and your money could grow to $40,354, potentially earning you $26,554 in compound interest.

- After 30 years, you will have contributed $16,560, and your money could grow to $62,532, potentially $45,972 in compound interest.

- After 35 years, you will have contributed $19,320, and your money could grow to $95,118, potentially earning you $75,808 in compound interest.

- After 40 years, you will have contributed $22,080, and your money could grow to $142,999, potentially earning you $120,919 in compound interest.

Tips for investing on a tight budget

If you are on a tight budget and want to maximize the little amount of money that you have to invest, here are two tips to make the most out of the money you have:

1. Get your employer match.

Your first money move should be to take advantage of your employer match. If your employer offers a retirement account plan, you should check if your employer offers to match a portion of your contributions.

The beauty of getting your employer match is that you don’t have to invest a lot of money to get it. An employer match is free money that could potentially grow to hundreds of thousands of dollars over the course of decades. Getting your employer match is one of your most powerful wealth-building tools.

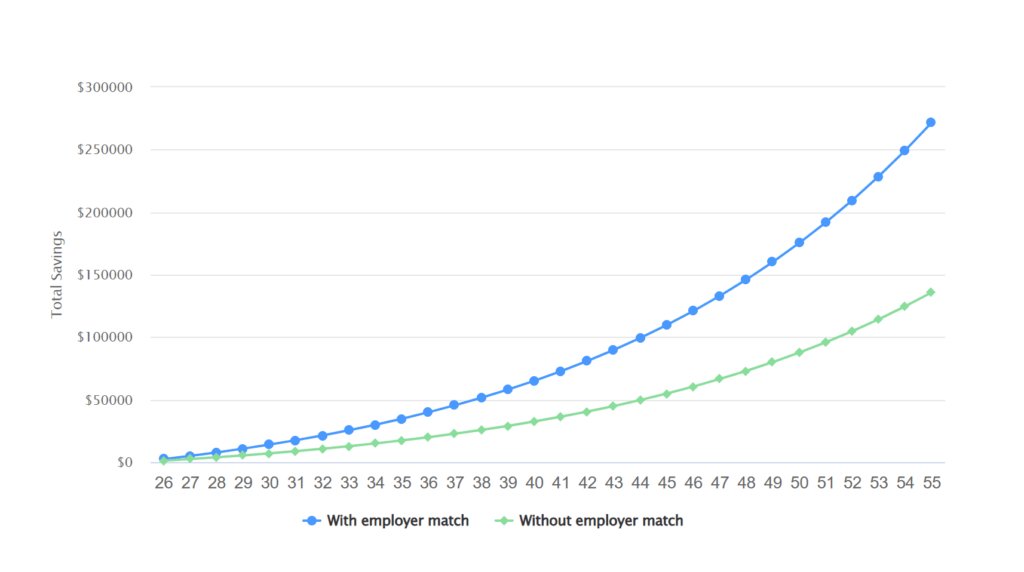

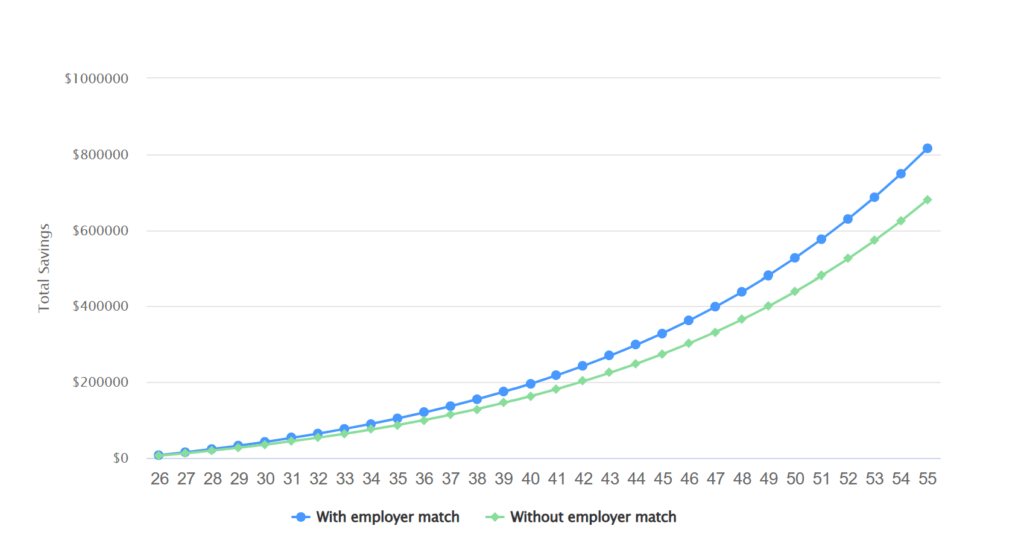

Here’s how it works: Your employer offers to match a percentage (for example, 50% or 100%) of your contribution up to a certain percentage of your salary, say 3%. Here’s what that looks like with specific numbers:

Scenario 1: If you make $40,000 a year and start by investing 3% of your salary (which is $100 a month or $1,200 a year) into your retirement plan, and you get a 100% employer match up to that 3%, then that means you invest $100 a month (or $1,200 a year) and your employer contributes $100 a month (or $1,200 a year) as well. In this scenario, because you contributed 3% and you got your 3% employer match, it’s really like you’re investing 6%.

Scenario 2: Let’s assume that you make $40,000 a year and get a 100% match up to 3% of your salary. In this scenario, you invest 15% of your income, then your employer would still only contribute 3% because that’s the maximum that your employer would contribute. So with your employer match, it’s like you’re investing 18% instead of 15%.

That extra 3% could make a massive difference to your financial future. If you contribute 15% of a $40,000 salary toward your retirement account and get a 3% employer match, your money could grow to $815,639 after 30 years of investing if you get an 8% rate of return. But without that employer match, your balance could fall to $679,699. By getting your employer match, you have the potential to gain $135,940 in compound interest:

Getting your employer match is an easy way to boost your investment rate and to get more for your money even if you can only invest a little bit. You can use this employer match calculator to see how much free money you could get per month with your employer match, and you can use Bankrate’s 401(k) calculator to see how your money will grow over time both with and without your employer match.

2. Fractional shares make investing easy on a tight budget.

So many people think that you need to have thousands of dollars to get started with investing. That’s NOT true. You can invest as little as $1 at a time with fractional shares. Fractional shares are just like what they sound like: parts of a share of stock, ETF, or index fund, for example. Instead of buying the whole share, you can just buy part of it.

For example, if a share of one stock costs $50 but you only have $25 to invest, you can buy half a share of that stock. That’s a fractional share.

Put differently: Fractional shares are based on the dollar amount that you want to invest rather than the number of shares you want to buy, which is what makes investing so accessible to low-income earners and those who are on a tight budget.

The power of small actions compounds enormously over time.

If you’re a low-income or median-income earner, investing money even when it doesn’t seem to make a difference and incrementally increasing your investment contributions by 1% at a time can be one of your most powerful wealth-building tools.

Gradually increasing your investment contributions by 1% repeatedly over time could lead to compound enormously to bring you tens of thousands or even hundreds of thousands of dollars in compound interest over the course of several decades.

If you shift your mindset from thinking that what you have is too little to invest to believing that every dollar counts, you’ll be surprised at just how much progress you can make toward your investing goals. Contribute what you can toward your retirement even if it’s just a few dollars and make today 1% better than yesterday.

1 thought on “How to Change Your Financial Life Through Incremental Progress”

Comments are closed.