Although you should strive to invest at least 20% of your income for retirement, investing 20% might not always be doable. The good news is that you could still make massive progress toward financial freedom by investing just 3% more of your income.

If you earn $30k to $55k a year, investing 3% more of your income starting in your 20s or 30s could help you build substantial wealth by the time you turn 62.

Investing 3% more on a $30,000 income

If you earn $30k a year, investing 20% of your income is just not possible unless you split your housing expenses with a roommate or partner. But if you can invest anything at all—even 3% of your income—your contributions could massively help you out on your path toward financial freedom.

The reason that you could still build wealth on a low income is that your most valuable asset is time, not money: The longer your money is invested, the more money you have.

If you earn $30,000 a year and invest $75 more a month—just 3% of your gross income—starting in your 20s, you could have an extra $231k to $580k by the time you turn 62 if you average a 10% rate of return:

If you’re in your 30s, unfortunately your money won’t grow as dramatically as it would have if you started investing 3% more in your 30s. However, you could still build meaningful wealth if you make this change in your 30s.

If you invest $75 more a month—just 3% of your gross income if you earn $30k a year—starting in your 30s, you could have an extra $79k to $208k by the time you turn 62 if you average a 10% rate of return:

But if investing 3% is too much, investing 2% of your income ($50 a month) or even 1% of your income ($25 a month) could still help you on your path to financial freedom.

Investing 3% more on a $35,000 income

If you earn $35,000 a year, investing 20% of your income will be difficult if not impossible unless you have an ultra low cost of living and/or you split housing expenses with a roommate or partner.

But if you can afford to invest anything at all, you could skyrocket your future retirement savings and make massive progress toward financial freedom.

The reason that you could build wealth on a low income is that time, not money, is your most important wealth-building tool: The amount of time that your money is invested matters more when it comes to building wealth than the amount of money you invest. So you don’t need a high income to become financially independent.

If you earn $35,000 a year and invest about $87 a month—just 3% of your gross income—starting in your 20s, you could have an extra $268k to $673k by the time you turn 62 if you average a 10% rate of return.

And if you’re in your 30s and earn $35k a year, investing 3% more of your income could still help you boost your progress toward financial freedom, especially if you make this change in your early 30s.

If you invest about $87 more a month—just 3% of your gross income if you earn $35k—starting in your 30s, you could have an extra $92k to $242k by the time you turn 62 if you average a 10% rate of return:

But if investing 3% is too much, you still could skyrocket your retirement savings if you invest just 2% more of your income ($58.34 a month) or even 1% more of your income ($29.17 a month).

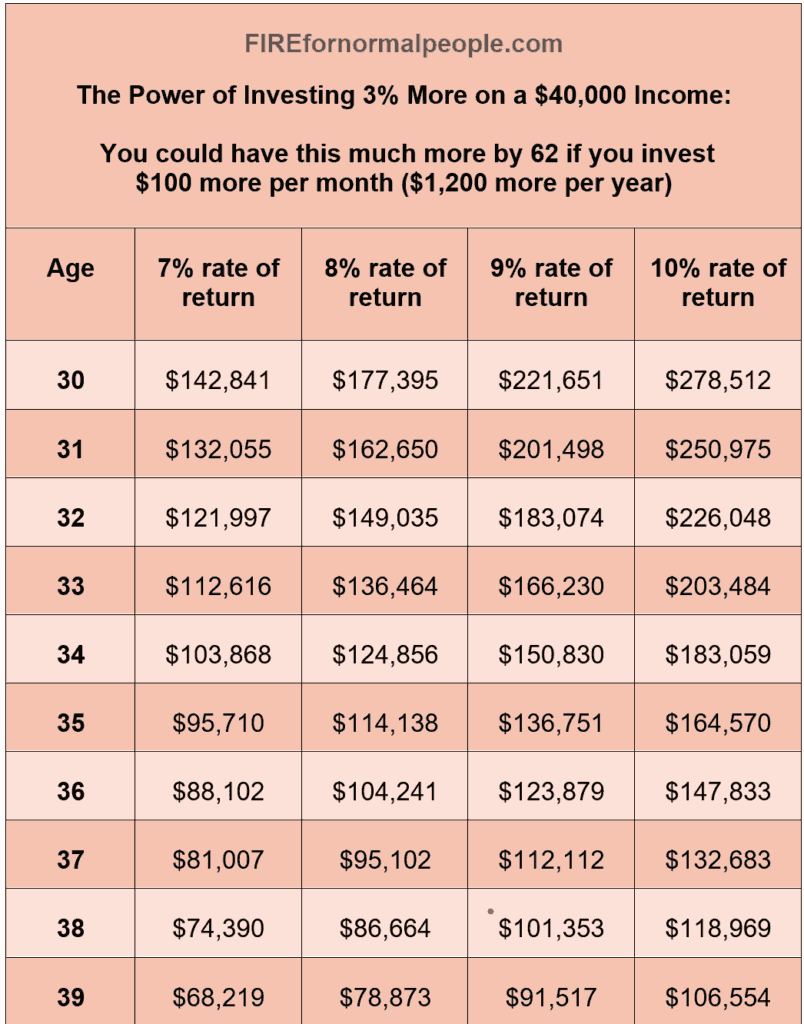

Investing 3% more on a $40,000 income

If you earn $40,000 a year, you have enormous potential to build long-term wealth and make substantial progress toward financial independence, even if you can’t yet invest 20%+ of your income.

If you invest $100 more a month—3% of your income if you earn $40,000 a year—starting in your 20s, you could have an extra $308k to $774k by the time you turn 62 if you average a 10% rate of return:

And if you’re in your 30s, investing $100 more a month could mean having an extra $106k to $278k by the time you turn 62 if you average a 10% rate of return:

Investing 3% more on a $45,000 income

If you earn $45k a year, you should be really excited about what investing 3% more could do for you, especially if you’re in your 20s or early 30s. Making this small change could make an unimaginable difference to your future wealth if you start investing early.

If you invest about $112 more a month—just 3% of your gross income if you earn $45k a year—starting in your 20s, you could have an extra $346k to $867k by the time you turn 62 if you average a 10% rate of return:

If you’re in your 30s and earn $45k a year, you could still have hundreds of thousand of dollars more by the time you reach your early 60s if you increase your investment rate by 3%.

If you invest about $112 more a month—just 3% of your gross income—starting in your 30s, you could potentially have an extra $119k to $311k by the time you turn 62 if you average a 10% rate of return:

Investing 3% more on a $50,000 income

If you earn $50k a year, investing 3% more of your income could be your secret weapon to skyrocket your retirement savings and make huge progress on your journey toward financial independence.

If you earn $50k a year and invest 3% more of your gross income—or $125 more a month—starting in your 20s, you could have an extra $386k to $968k by the time you turn 62 if you average a 10% rate of return:

If you earn $50,000 a year and invest 3% more of your gross income—or $125 more a month—starting in your 30s, you could have an extra $133k to $348k by the time you turn 62 if you average a 10% rate of return:

Investing 3% more on a $55,000 income

Investing 3% more of your income if you earn $55k a year could portially build a life-changing amount of wealth if you start investing early.

If you earn $55k a year and invest 3% more of your gross income—or about $137 more a month—starting in your 20s, you could have an extra $423k to $1 million by the time you turn 62 if you average a 10% rate of return:

Even if you’re in your 30s, investing 3% more on a $55k salary could help you make incredible progress toward financial independence.

If you earn $55,000 a year and invest 3% more of your gross income—or about $137 more a month—starting in your 30s, you could have an extra $145k to $381k by the time you turn 62 if you average a 10% rate of return:

Is investing 3% more enough?

Ultimately, you should invest at least 20% of your income for retirement, so you don’t want to stop at investing just 3% more unless you’ve already met this goal and are on track with your investing goals.

However, that 3% could make the difference between being able to retire early/on time or needing to work for several more years. If you procrastinate on investing because you don’t think that 3% is good enough, you could end up missing out on hundreds of thousands of dollars by the time you retire—even if you earn a lower income.

1 thought on “The Power of Investing 3% More”

Comments are closed.