Reaching $100k in investments as soon as possible is your most important financial goal, but reaching your first $100k can often feel impossible. However, this goal is more achieveable if you break it down into smaller, more manageable steps, like reaching your first $10,000 milestone. Because of the power of compound interest, if you can invest your first $10,000, you’ll be well on your way to reaching your $100k investing goal.

This guide will show you the specific numbers behind why saving your first $10,000 matters for building long-term wealth, how to save you first $10,000 even if you earn a low income, and how saving your first $10,000 helps you reach your $100k investing goal.

How investing your first $10,000 helps you build long-term wealth

Investing your first $10,000 is an incredible first step to building long-term wealth—especially if you start investing in your 20s or early 30s. That’s why you should feel proud of any progress you can make toward this milestone.

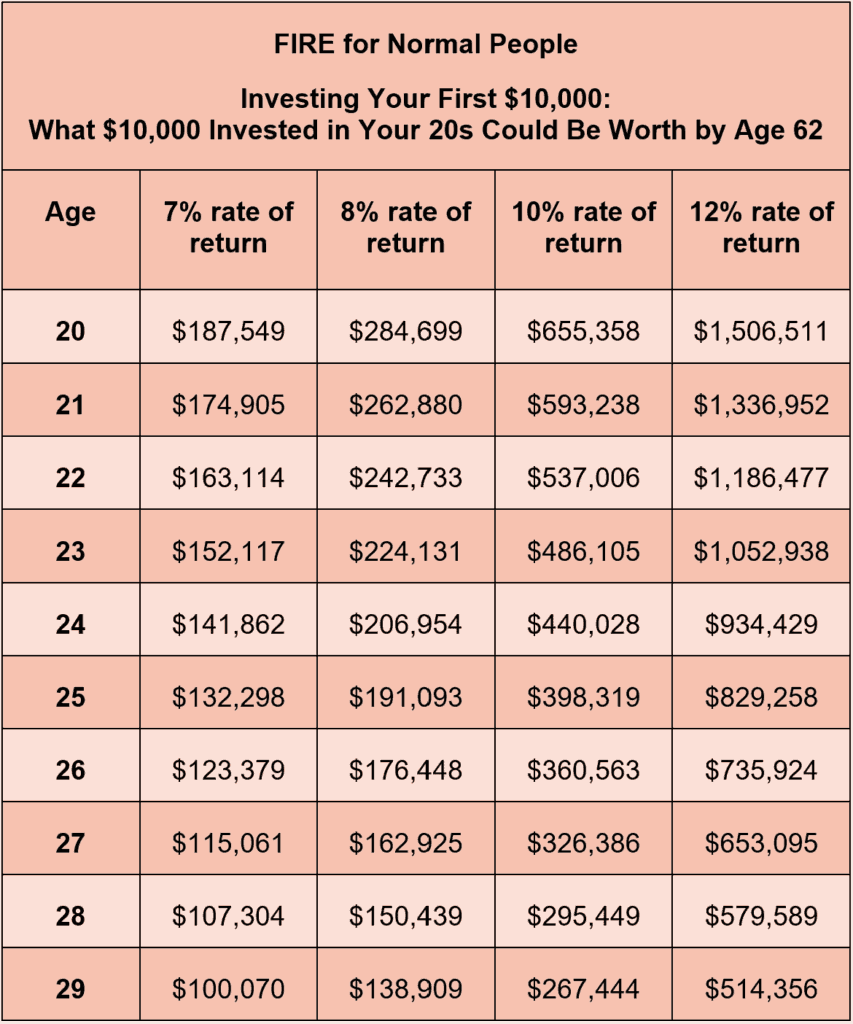

If you can invest your first $10,000 in your 20s, that could potentially grow to hundreds of thousands of dollars or even over 1 million dollars by the time you reach age 62, depending on your rate of return and the age you start investing:

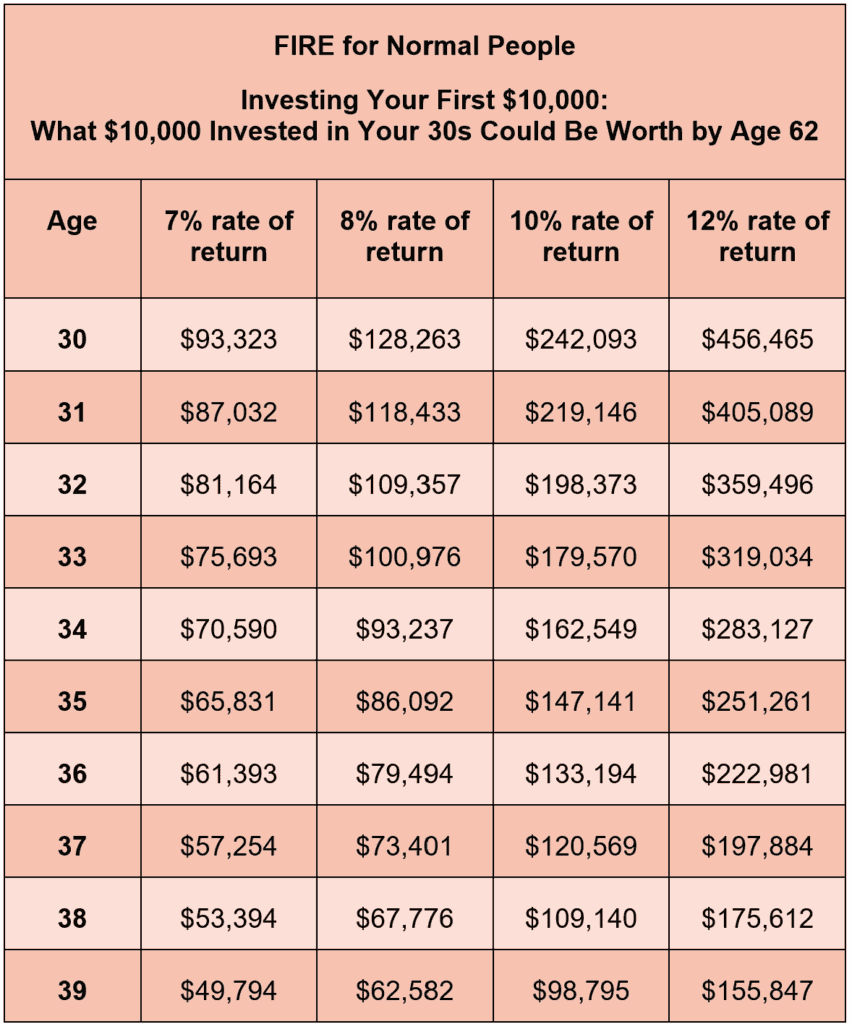

And if you invest your first $10,000 in your 30s, that money could still potentially grow to over $100,000 by the time you turn 62:

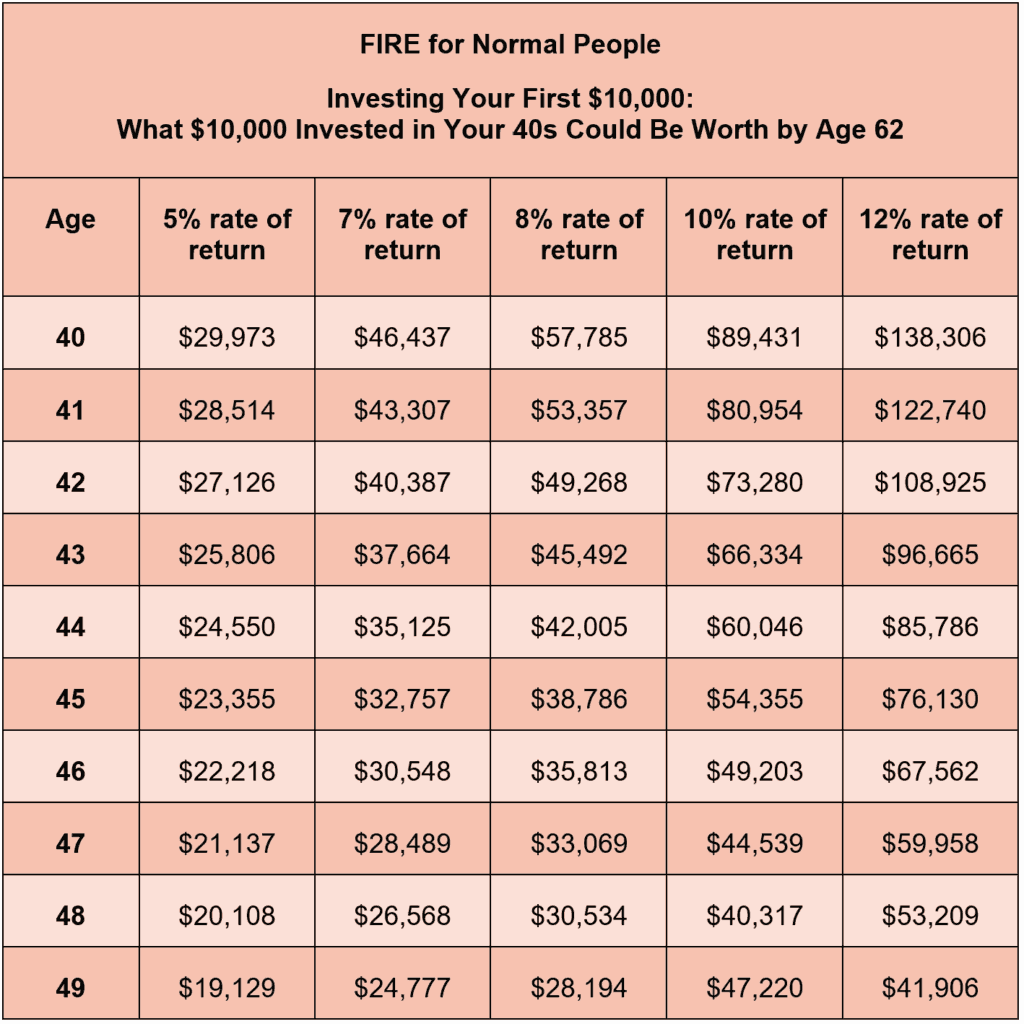

And while your money won’t grow as much if you’re a first-time investor in your 40s, that initial $10,000 still has the potential to grow to tens of thousands of dollars by the time you reach age 62:

How your first $10,000 helps you reach your $100k investing goal

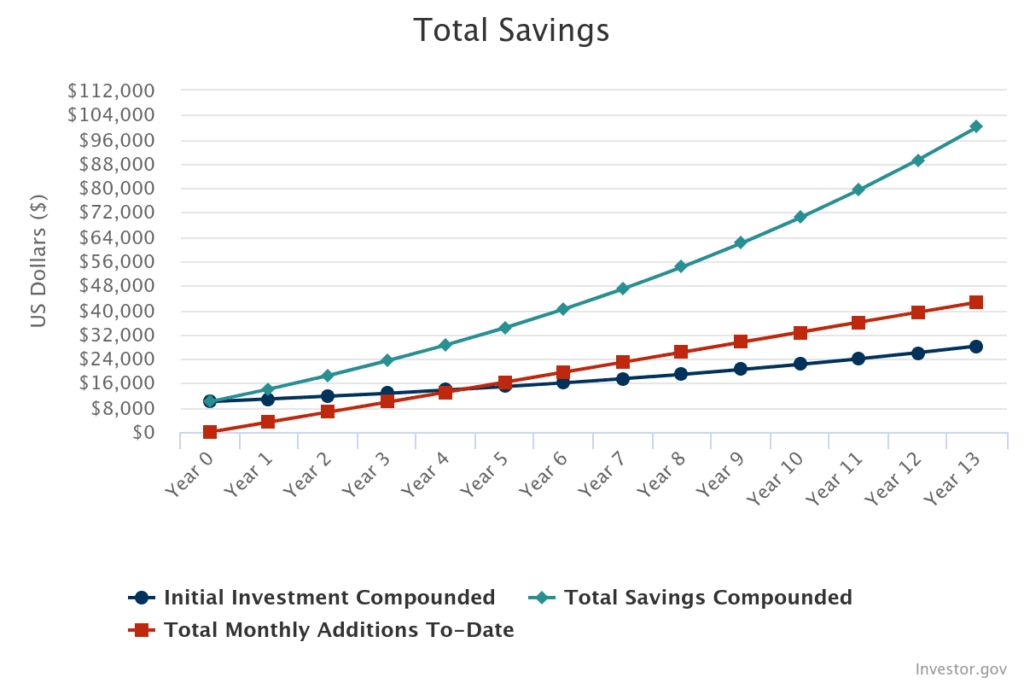

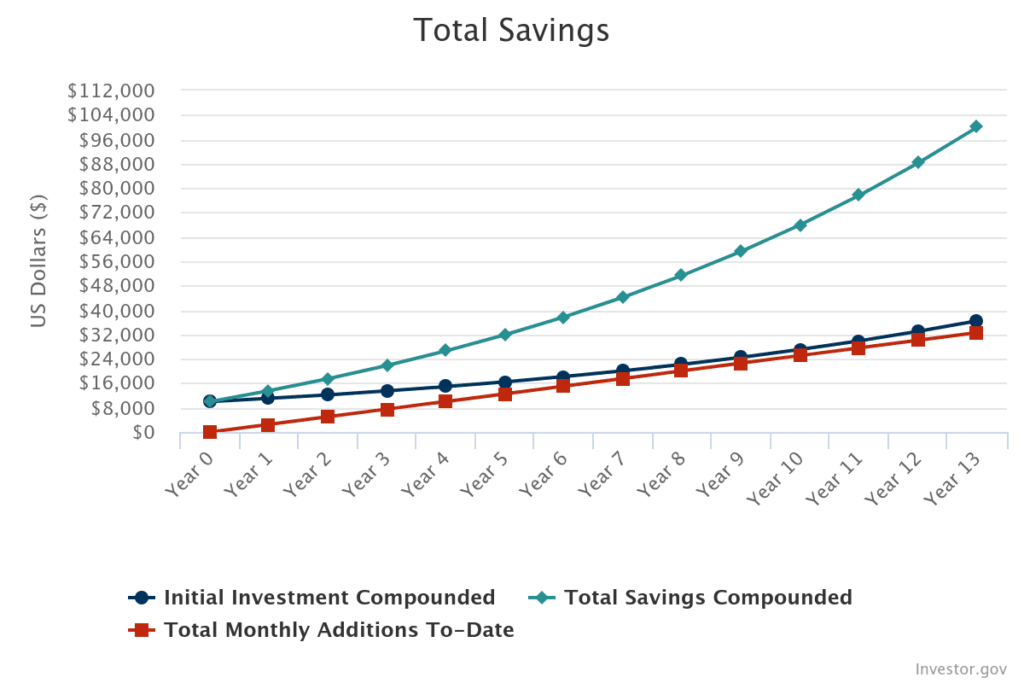

If you invest your first $10,000 and want to reach your $100k investing goal in the next 13 years, that initial $10,000 could grow to $28,194 by the end of 13 years if you get an 8% rate of return. In this scenario, that initial $10,000 helped you reach 28% of your $100k investing goal:

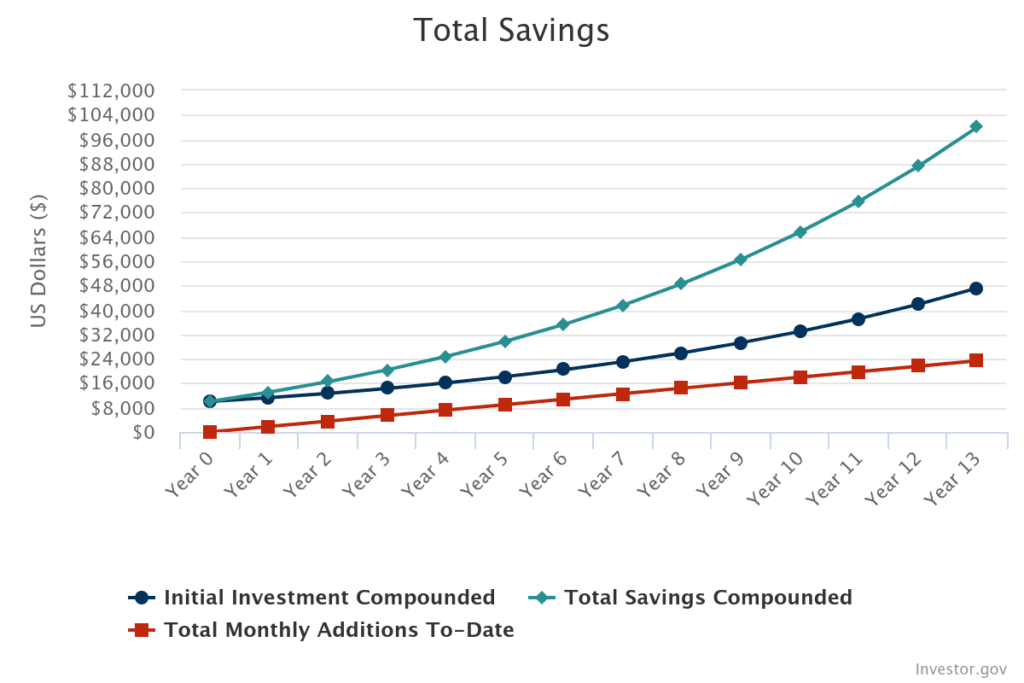

And if you get a 10% rate of return, that initial $10,000 could grow to $36,495 after 13 years, helping you reach 36% of your $100k investing goal:

Finally, if you get a 12% rate of return, that initial $10,000 could grow to $47,220 after 13 years, helping you reach an incredible 47% of your $100k investing goal:

How to save your first $10,000

Traditional savings challenges

If you already have room in your budget for saving and investing after you pay your necessary expenses, then you might want to try a savings challenge to meet this $10,000 goal. Here’s how you can meet that investing goal if you get paid weekly, bi-weekly, or monthly:

If you get paid weekly…

- To save $10,000 in 2 years (100 work weeks), you would have to save $100 per paycheck.

- To save $10,000 in 2.5 years (126 work weeks), you would have to save $80 per paycheck.

- To save $10,000 in 3 years (150 work weeks), you would have to save $67 per paycheck.

- To save $10,000 in 3.5 years (176 work weeks), you would have to save $57 per paycheck.

- To save $10,000 in 4 years (200 work weeks), you would have to save $50 per paycheck.

If you get paid bi-weekly…

- To save $10,000 in 2 years (100 work weeks), you would have to save $200 per paycheck.

- To save $10,000 in 2.5 years (126 work weeks), you would have to save $159 per paycheck.

- To save $10,000 in 3 years (150 work weeks), you would have to save $134 per paycheck.

- To save $10,000 in 3.5 years (176 work weeks), you would have to save $114 per paycheck.

- To save $10,000 in 4 years (200 work weeks), you would have to save $100 per paycheck.

If you get paid monthly…

- To save $10,000 in 2 years, you would have to save $417 per month.

- To save $10,000 in 2.5 years, you would have to save $334 per month.

- To save $10,000 in 3 years, you would have to save $278 per month.

- To save $10,000 in 3.5 years, you would have to save $239 per month.

- To save $10,000 in 4 years, you would have to save $209 per month.

Reverse savings challenges

If you earn a low income, you might want to do a reverse savings challenge instead of a traditional savings challenge.

Instead of telling you how many dollars to save per paycheck, per week, or per month, a reverse savings challenge tells you how many more hours per week you would have to work to meet your savings goal, depending on your hourly wage and goal deadline.

Traditional savings challenges already presume that you already have extra money leftover after your essential bills, which is not the reality for many lower-income earners. For most low-income earners, saving more doesn’t mean cutting back on your expenses—it means adding more hours to your work week (or switching jobs to get a pay raise).

I love reverse savings challenges because they feel so much more actionable if you earn a low income: While cutting your expenses to save $200 a month is often impossible on a low income, working an extra 3–4 hours a week feels a lot more approachable.

The following reverse savings challenges assume an extra 12% cushion to account for taxes:

If you make $17 an hour…

- To save $10,000 in 2 years, (100 work weeks), you would have to work 6.69 more hours per week.

- To save $10,000 in 2.5 years (126 work weeks), you would have to work 5.31 more hours per week.

- To save $10,000 in 3 years (150 work weeks), you would have to work 4.46 more hours per week.

- To save $10,000 in 3.5 years (176 work weeks), you would have to work 3.80 more hours per week.

- To save $10,000 in 4 years (200 work weeks), you would have to work 2.95 more hours per week.

If you make $15 an hour…

- To save $10,000 in 2 years (100 work weeks), you would have to work 7.58 more hours per week.

- To save $10,000 in 2.5 years (126 work weeks), you would have to work 6.02 more hours per week.

- To save $10,000 in 3 years (150 work weeks), you would have to work 5.06 more hours per week.

- To save $10,000 in 3.5 years (176 work weeks), you would have to work 4.31 more hours per week.

- To save $10,000 in 4 years (200 work weeks), you would have to work 3.79 more hours per week.

If you make $12 an hour…

- To save $10,000 in 2 years (100 work weeks), you would have to work 9.47 more hours per week.

- To save $10,000 in 2.5 years (126 work weeks), you would have to work 7.52 more hours per week.

- To save $10,000 in 3 years (150 work weeks), you would have to work 6.32 more hours per week.

- To save $10,000 in 3.5 years (176 work weeks), you would have to work 5.39 more hours per week.

- To save $10,000 in 4 years (200 work weeks), you would have to work 4.74 more hours per week.

What to do if saving $10,000 is too difficult?

If saving your first $10,000 still feels too overwhelming on a low wage, I highly recommend starting with saving your first $1,000 or your first $5,000 instead—you would be surprised at how attainable those goals are if you do a reverse savings challenge. And if you can save $1,000 or $5,000, then reaching your $10,000 milestone will start to feel much more approachable.

Here are some articles to get you started with more manageable goals:

- Invest Your First $100k Step-by-Step: How to Save Your First $1,000

- Invest Your First $100k Step-by-Step: How to Save Your First $5,000

Reaching your $100k investing goal may seem daunting, but if you can just reach that first $10,000 milestone, you could give yourself a massive boost toward your $100k goal. You should be so proud of yourself for making progress toward that $10,000 milestone because you’re laying the groundwork for building massive wealth in the future.