If you want to know how to build wealth on a lower income, here’s the secret: You’ve got to invest what you can now. Your money grows much more efficiently if you invest what you can now instead of waiting years until you earn more to start investing. That’s because your most powerful wealth-building tool is the length of time that your money is invested—not necessarily how much you invest.

Investing smaller amounts consistently over a longer period of time could potentially grow your wealth more—and more efficiently—than investing larger amounts over a shorter period of time. Even investing $100/month could potentially build more wealth than investing $1,000/month if you invest your money longer.

Here are three examples to show that sometimes less is more when it comes to investing:

Investing $100 a month for 25 years vs. investing $1,000 a month for 5 years

If you invest $100 a month for 25 years and average a 10% rate of return, you could have about $132,683 by the end of those 25 years. In this scenario, you invested only $30,000 of your own money, but you ended up with $132,683 because of how long your money was invested. Here, your money grew by $102,683, which is 2.42x the amount you originally invested:

In contrast, if you invest $1,000 for 5 years and get a 10% rate of return, you could have $77,437 by the end of those 5 years. However, your own contributions would total $60,000. In this scenario, your money only grew by $17,437, which is just 29% of your total contributions:

This first set of examples shows you how sometimes less is more when it comes to investing.

In the second scenario where you invested $1,000 a month for 5 years, you actually contributed $30,000 more than the first scenario where you invested $100 for 25 years, but you still ended up with less money overall—$55,246 less—because your money didn’t have enough time to grow.

Building wealth is more about how long your money is invested than how much you invest—which is why you could potentially build more wealth by investing $100 a month than by investing $1,000 a month.

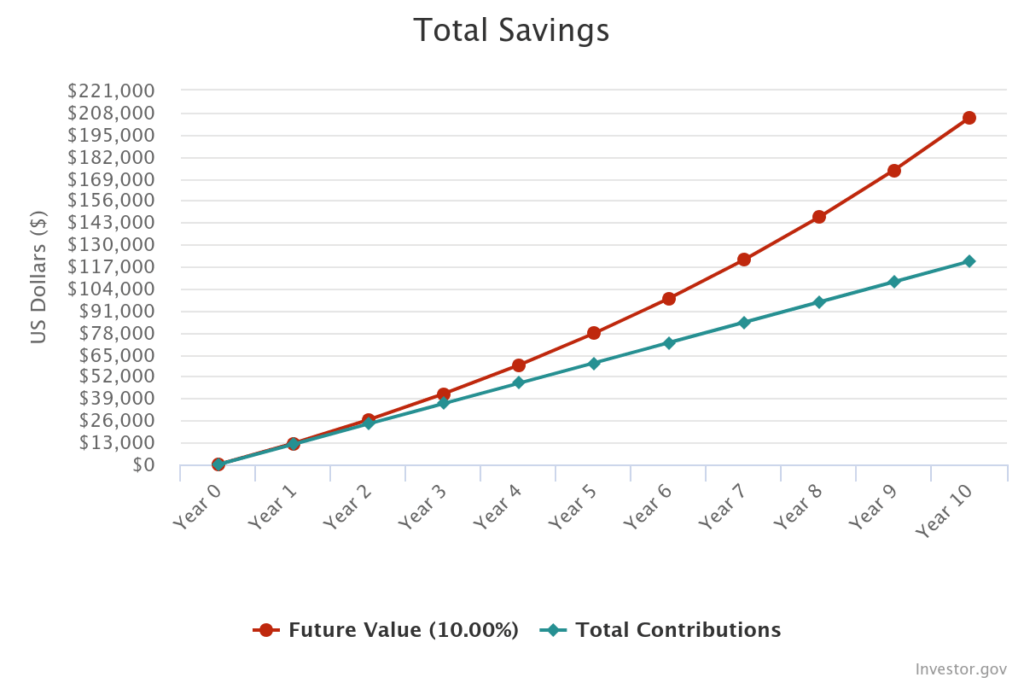

Investing $100/month for 30 years vs. investing $1,000/month for 10 years

If you invest $100 per month for 30 years and you get a 10% rate of return, you could have $226,048 at the end of those 30 years. Only $36,000 of that $226,048 would be money that you contributed toward this goal—in other words, your money grew by $190,048, which is 5.28x the original amount you invested:

In contrast, if you invest $1,000 per month for 10 years and you get a 10% rate of return, you could have $204,844 at the end of those 10 years. And $120,000 of that $204,844 would be money that you contributed. In this scenario, your money grew by only 70%.

This second set of examples shows the power of small, consistent investments over a long period of time.

In the second scenario where you invested $1,000 a month for 10 years, you actually contributed $84,000 more than the first scenario where you invested $100 for 30 years, but you still ended up with less money overall—$21,204 less—because your money was invested for a shorter period of time.

Not only could you have more money in the first scenario where you invest $100 a month—it’s so much more efficient to invest smaller amounts of money for longer periods of time than larger amounts over a short period of time.

Investing $100/month for 40 years vs. investing $1,000/month for 15 years

This third set of examples shows the true power of delayed gratification and small, consistent actions over a long period of time.

If you invest just $100 for 40 years and get a 10% rate of return, you could have $632,407 at the end of that time period, and only $48,000 would be money that you contributed. That’s a growth of $584,407, which is 12.18x the amount you originally invested:

In contrast, if you invest $1,000 a month for 15 years and get a 10% rate of return, you could have $414,470 by the end of that time period. After 15 years, your contributions to total $180,000, so your money grew by $234,470. But while that it is a lot of money, it’s only 1.3x the amount that you contributed:

In this first scenario where you invested $100 a month, you not only ended up with more money overall—$217,937 more—but your money also grew more efficiently. You invested only $48,000 of your own money, but you ended up with $632,407 after 40 years.

But in the second scenario where you invested $1,000 a month, you invested $180,000 and ended up with $414,470 after 15 years. Again, this shows you that time—not money—is your most powerful wealth-building tool.

You don’t need a high income to build wealth.

These examples show you that you don’t need to invest $1,000 a month or more to start building wealth. You can start with where you’re at. Even investing $100 a month (if that’s all you can afford) could make a massive difference to your net worth over decades.

Investing what you can right now is just working smarter, not harder. If you delay investing until you earn a high income, you’re just going to have to work so much harder to achieve a goal you could have achieved much more easily if you would have started investing sooner with smaller, more manageable amounts.

The true path to wealth creation for the average person is investing what you can on a regular basis and investing early in life. If you make a low or average income, you can’t afford to wait around until you earn a higher income: You have to decide to take advantage of your most powerful wealth-building tool—time—and invest what you can right now, even if it’s just $5, $20, $50, or $100.