If you’re like 57% of Americans and keep your savings in a checking account or traditional savings account instead of a high-yield savings account, you’re missing out on the opportunity to earn hundreds or even thousands of dollars in free money and have your savings outpace inflation. If you earn a lower income, you’ll want to take advantage of this tool to help skyrocket your savings and meet your savings goals faster.

Read on to see the hard numbers behind how a high-yield savings account can help skyrocket your savings:

What is a high-yield savings account and how does it work?

A high-yield savings account is just a savings account where your money earns much more interest than a traditional savings account—and the more interest your account earns, the more money you have.

High-yield savings accounts are typically available at online banks and are less common at traditional banks with brick-and-morter locations. Because online banks have lower operating costs than brick-and-morter banks, they’re able to offer more competitive interest rates on their savings accounts.

The beauty of a high-yield savings account is that not only does your money earn more interest than a typical savings account—your money actually earns compound interest, meaning that the interest your money generates actually creates its own interest.

If your money sits in a regular savings savings account, you’re not only missing out on higher compound interest rates—you’re not even earning enough interest on your account to outpace inflation. This means that your money is losing buying power—in other words, the cost of living will continue to increase while your account balance stays basically the same.

High-yield savings accounts outperform regular savings accounts.

Regular savings accounts currently earn about 0.61% interest, while the current rate of inflation is 2.3%. And while that small percentage may not sound like a big deal in the short-term, over the medium-term and long-term, not using a high-yield savings account could result in your money losing significant value.

If the money loses about 2.5% of its purchasing power each year, after 10 years, that means that your money is worth about 25% less than when you first put it in that account. That’s why it’s so important for your money to outpace inflation.

A high-yield savings account lets your money do exactly that. High-yield savings accounts earn interest rates of anyhwere from about 3.5% to just over 5%, which means that your money actually grows substantially over time.

Let’s see how this actually means for your savings:

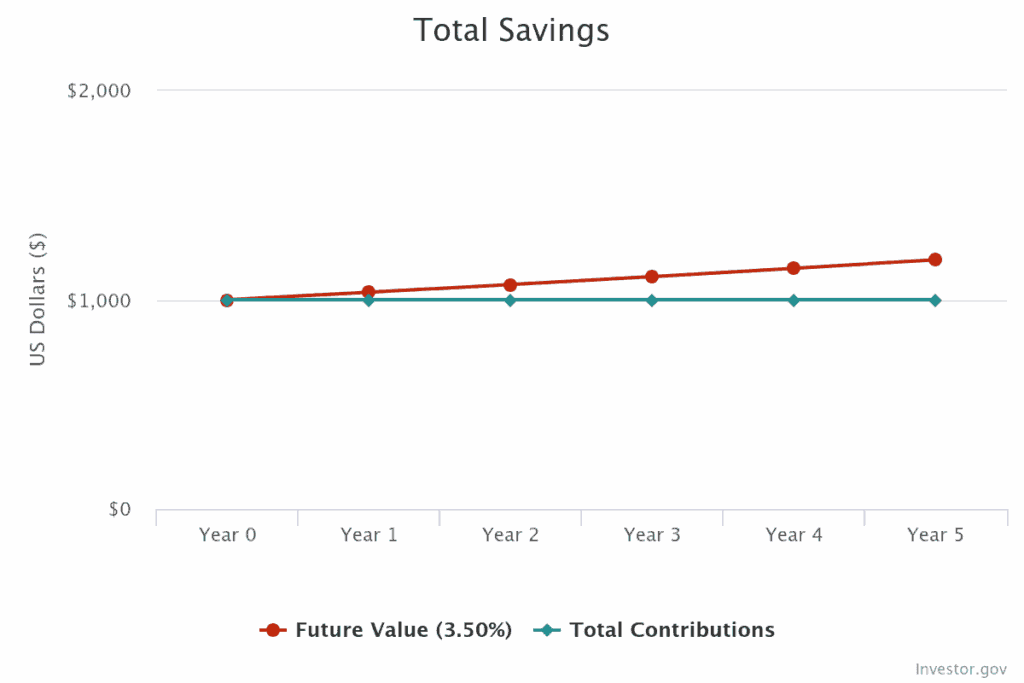

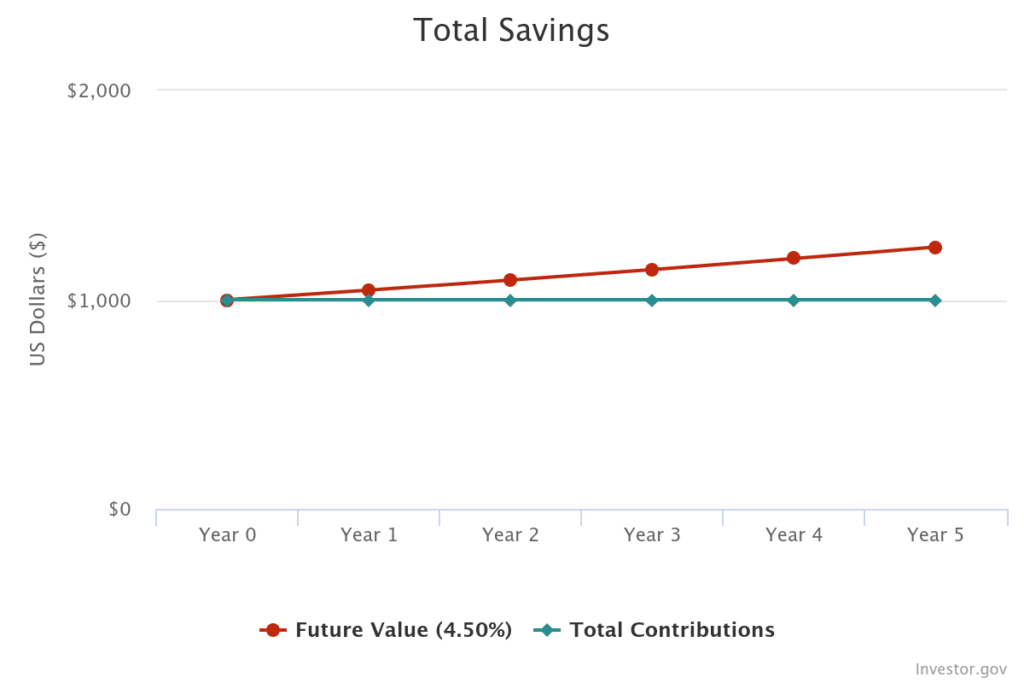

Saving $1,000: High-yield savings account vs. regular savings account

High-yield savings account

If you put $1,000 in a high-yield savings account and you get an interest rate of 3.5%, that $1,000 could grow to $1,190 after 5 years. In other words, your savings could grow by 19% just by just parking it in a high-yield savings account—that’s a lot of extra money if you’re just getting started with your savings journey.

Or if you get an average interest rate of 4.5%, that $1,000 could grow to $1,251 after 5 years. That’s an increase of 25% just because you put your money in a high-yield savings account:

Regular savings account

If you put $1,000 in a regular savings account that gets an interest rate of 0.61%, that $1,000 could grow to just $1,030.50 after 5 years.

In other words, if you put $1,000 in a regular savings account instead of a high-yield savings account with a 3.5–4.5% interest rate, you could miss out on $159.50–$220.50 after 5 years.

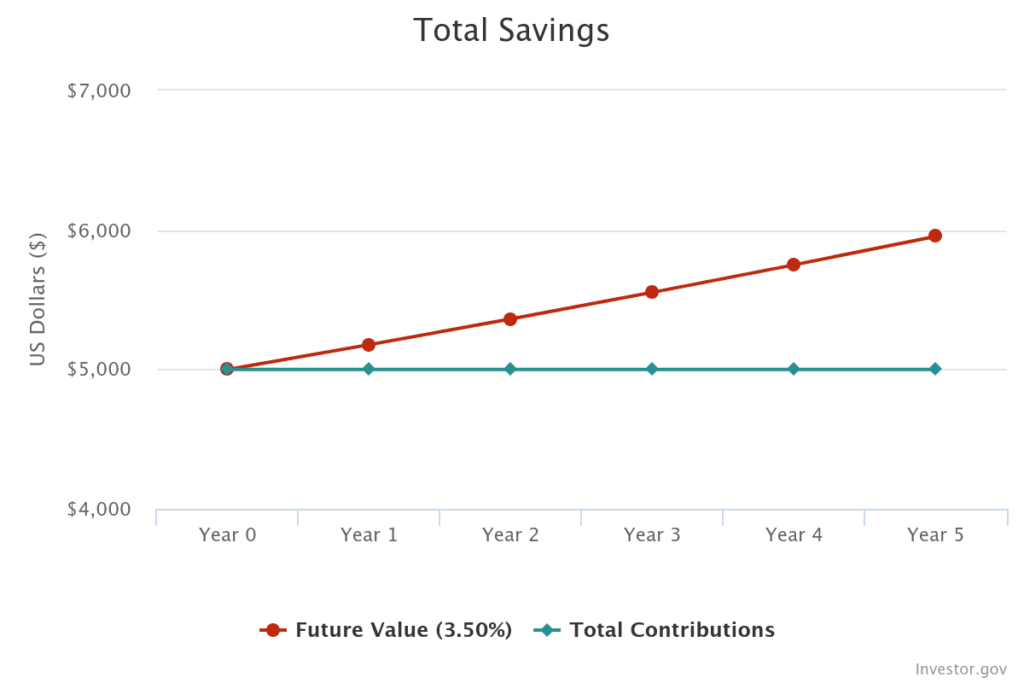

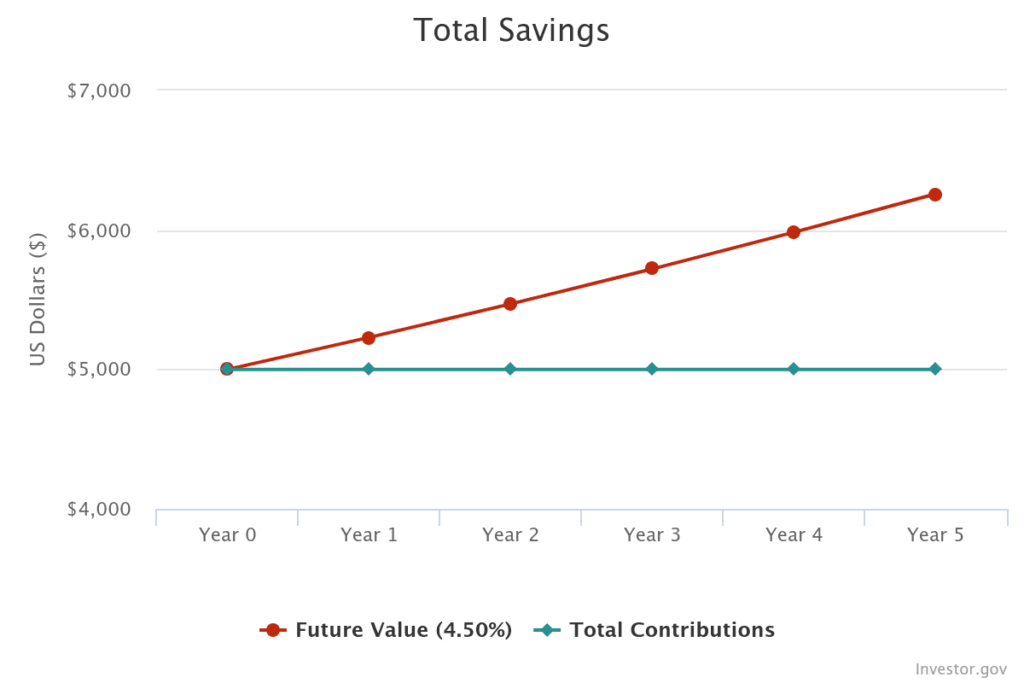

Saving $5,000: High-yield savings account vs. regular savings account

If you put $5,000 in a high-yield savings account and you get an average interest rate of 3.5%, that $5,000 could grow to $5,954 after 5 years. Putting that money in a high-yield savings account let you grow your money by 19%:

And if you get a 4.5% interest rate, that $5,000 could grow to $6,258 after 5 years—an increase of 25%:

Regular savings account

If you put $5,000 in a regular savings account that gets an interest rate of 0.61%, that $5,000 could grow to just $5,152.50 after 5 years.

In other words, if you put $5,000 in a regular savings account instead of a high-yield savings account with a 3.5–4.5% interest rate, you could miss out on $801.50–$1,105.50 after 5 years.

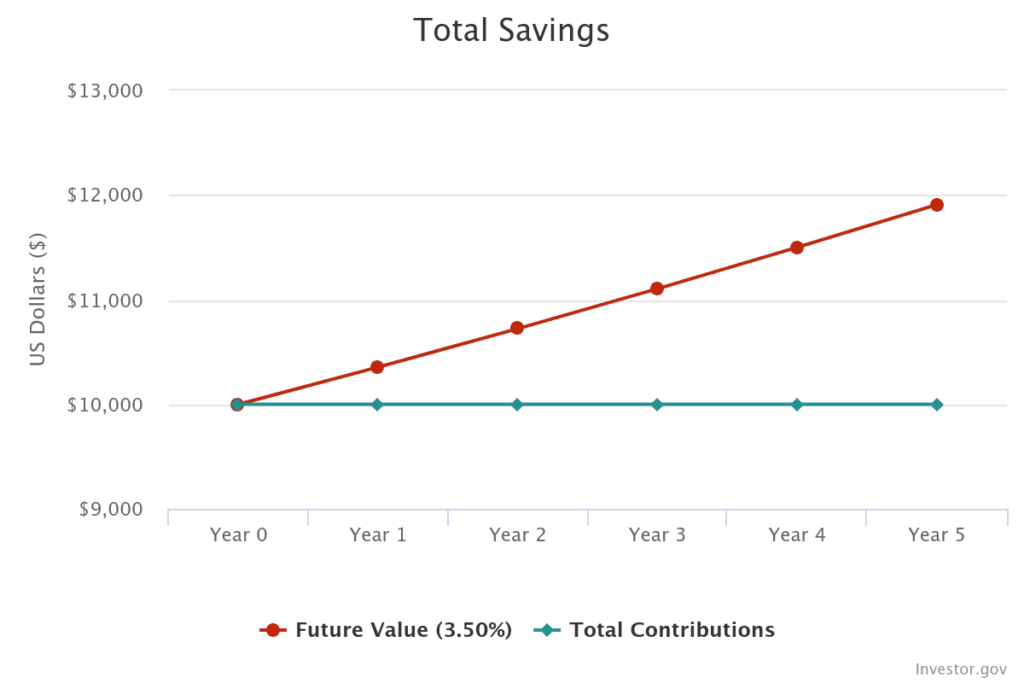

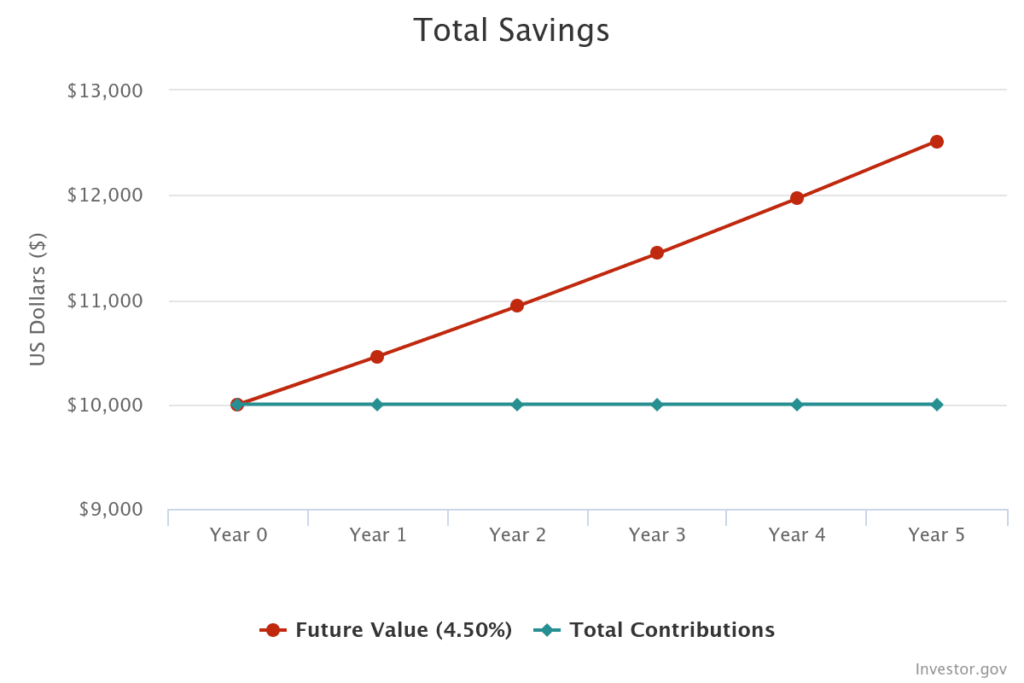

Saving $10,000: High-yield savings account vs. regular savings account

If you put $10,000 in a high-yield savings account that has an interest rate of 3.5%, after 5 years, that $10,000 could grow to $11,909. In other words, you could grow your savings by 19% just by putting it in a high-yield savings account:

Or if you get a 4.5% interest rate, that $10,000 could grow to $12,517 after 5 years. In this scenario, your money could grow by 25% just because you put it in a high-yield savings account:

Regular savings account

If you put $10,000 in a regular savings account for 5 years, that $10,000 could grow to just $10,305 at the end of that time period.

By placing that $10,000 into a regular savings account instead of a high-yield savings account with a 3.5–4.5% interest rate, you could miss out on $1,604–$2,212 after 5 years.

What to use a high-yield savings account for?

You should keep your emergency fund—at least 3 to 6 months of expenses—in a high-yield savings account. A high-yield savings account is also an optimal place to keep money for short-term or medium-term goals, like buying a car or saving up for a down payment on a house.

A high-yield savings account allows you to have the benefit of letting your money grow while still remaining easily accessible in a low-risk account.

If you don’t already have a high-yield savings account, you’re missing out on the opportunity to earn free money and have your money outpace inflation. A high-yield savings account can help skyrocket your savings, which is why you absolutely should have one if you earn a lower income.

1 thought on “Why You Need a High-Yield Savings Account”

Comments are closed.